The Central Bank of Iceland publishes Monetary Bulletin and lowers interest rates

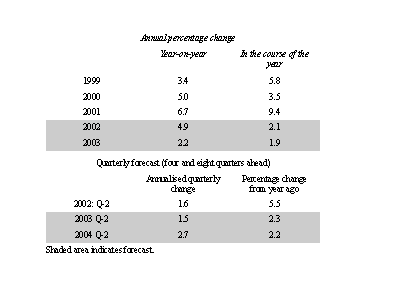

On August 1, 2002, the Central Bank of Iceland published the August issue of Peningamál (Monetary Bulletin), including the Bank's quarterly inflation forecast. Continued appreciation of the króna and a cooling economy are expected to lead to rapidly declining inflation this year with the Central Bank's 2.5% inflation target being attained in the fourth quarter of the year, a year earlier than envisaged in the inflation forecast issued in May 2002 and when the inflation targeting regime was adopted in March 2001. According to the new forecast, inflation will decline more rapidly than previously expected and be 2.3% over the next four quarters. The Bank forecasts inflation over the course of 2002 to be 2.1%. The outlook for 2003 is similar to the one in the last issue of Monetary Bulletin. Inflation two years ahead is forecast to be 2.2%, given an unchanged monetary stance.

On the basis of this forecast the Board of Governors of the Central Bank of

Iceland decided to lower the yield in the Bank's repurchase transactions with

credit institutions by 0.6 percentage points, to 7.9 percent, effective at the

next auction of repurchase contracts on August 6, 2002.

The

English translation of Peningamál, Monetary Bulletin, will appear on the Bank's

website, each chapter as soon as it becomes available. Attached is a preliminary

English translation of the Bulletin's introductory chapter.

Consumer price inflation in Iceland 1999 to 2004

{kind=link}

Central Bank inflation forecast

{kind=link}

Preliminary translation of the introductory chapter in the August 2002 issue of the Central Bank of Iceland's Monetary Bulletin:

Better macroeconomic balance and decreasing inflation create conditions for a further easing of the monetary stance

The imbalances that prevailed in Iceland's economy during the latter half of

the upswing have largely disappeared. Pressure in the goods and labour markets

has eased, the current account balance has moved well within sustainable limits

and inflation is rapidly on the decrease. The Central Bank's inflation target

could be attained before the end of the year. The fundamentals for economic

stability have therefore been restored. This creates conditions for an

acceptable rate of economic growth at the same time as inflation remains close

to the Central Bank's target.

The tight monetary stance of recent

times has played the greatest part in the success that has been achieved. High

interest rates reduced investment and private consumption, and bolstered the

exchange rate of the króna after pessimism gave way to confidence, when the

unions and employers agreed to postpone their review of wage agreements until

this May and tie it to a specific price level target. Lower demand in the goods

and labour markets and a stronger exchange rate then dampened inflation from

both domestic and foreign sources.

These changes in the macroeconomic

situation call for a new orientation of economic policy. Monetary policy must

ensure that the inflation target is attained, but as this comes closer to being

realised, conditions are created for addressing to some degree the low economic

growth rate and slack in the goods and labour markets. How big this slack will

turn out to be is still highly uncertain. While there are signs that demand for

goods and services has bottomed out, it cannot be stated absolutely that a

measurable upswing has begun. Considerable uncertainty also pertains as to

whether there will be a surge in corporate investment if no power-intensive

industrial investment materialises. Most of the signs suggest that the slack in

the labour market will intensify for the time being, however, since historical

and international experience show that it lags behind the general demand cycle.

The twelve-month rise in the CPI in June moved within the upper

tolerance limit of the Central Bank's inflation target for this year. This was

in line with the Bank's inflation forecast, which was fully realised in the

second quarter. On a shorter-term view, the underlying rate of inflation is

probably already consistent with the Bank's inflation target. At present it is

primarily domestic in origin. Inflation expectations in the bond market are also

in line with the Bank's target.

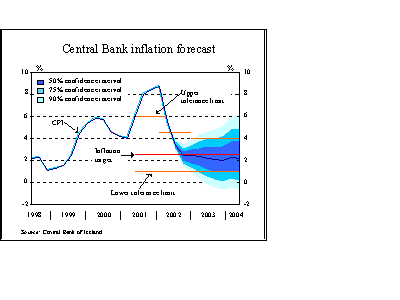

The inflation outlook has improved

since the Central Bank published its last inflation forecast, mainly due to the

strengthening of the króna. Assuming an unchanged exchange rate and monetary

stance, twelve-month inflation is now forecast to move within the long-range

tolerance limit of the inflation target as early as the third quarter, and the

Bank's inflation target will be attained before the end of the year. Projected

two years ahead, inflation will fall below the Bank's target.

In

recent weeks the exchange rate of the króna has been relatively stable and

somewhat higher than in the spring. For some time now the Central Bank has

identified a need to strengthen its foreign position. Hitherto, however, it has

not purchased foreign currency in the market to this end, since the inflation

target has enjoyed absolute priority and the Bank has not wanted to jeopardise

the exchange rate. The Bank now considers that conditions are in place for

moderate currency purchases of this kind and will publicly announce its

intentions in that regard in the near future. It should be underlined that the

aim of currency purchases will be to boost the Bank's foreign position, not to

seek to maintain the exchange rate of the króna within specific limits.

The inflation forecast and analysis of the economic situation and

outlook presented here demonstrate that the fundamentals are in place for a

further reduction in the Central Bank's policy interest rate. The Central Bank

interest rate is now around 5½% in real terms and in fact higher based on a

one-year inflation projection. This is above the equilibrium real interest rate

and too high with respect to mounting slack in the economy. The Bank has

therefore decided to cut its interest rate in repo transactions by 0.6

percentage points. It will be reduced even further in the months to come if

subsequent events confirm that the inflation target will be attained and demand

develops along the lines currently foreseen. If demand grows faster than is

thought likely at the moment, however, the situation could naturally change.

Later, power-intensive industrial development could also fuel pressure in the

goods and labour markets, thereby calling for a timely response on the part of

the Central Bank. As argued in the following article in this edition of Monetary

Bulletin, however, the time has still not come for taking specific account of

these factors in the Central Bank's interest rate decisions.

Nr. 9/2002

August 1, 2002